A fresh approach to accountancy

Delivering valued accountancy services to ambitious businesses who aspire to drive their business forward.

Services

Financial data capture and processing

Accurate financial capture and processing helps you make those vital business decisions and run your business more smoothly. Whether you need accounting and bookkeeping support, or you want to outsource all your accounting, Purple Lime can help. We are paperless and cloud-based making all those processes much quicker.

Financial management information

Financial Management includes planning, making good use of funds and keeping your business financially stable. It can also help you decide where future profits might lie and where services may need to be realigned. An expert business accountant can help you make the right decisions for your business in real time with industry leading tools.

Corporate finance

Whatever stage your business is currently at, there will most likely be a need to develop, grow, reorganize, or appraise your business. Our team of specialists can provide valuable support and care in a number of complex areas within corporate finance including: management buyouts, EOTs, trade sales, mergers and acquisitions, CFO reports, equity funding, debt raising, valuation, planning, modelling and budgeting. It is important to work with someone you can trust to be able to access and analyse the information as well as advising on the right options for your business.

Outsourced finance director and business consulting

In our experience, any SME organisation can benefit from Finance Director input. This may require tactical advice on a part-time basis with your existing accounts department or on a more involved level with a full finance function. Purple Lime offer tailor made FD services to help your business understand figures, providing valuable insight which in turn will help you make informed decisions at the right time. Reviewing your data and forecasting competently eliminates hasty decisions and neglected growth opportunities.

Founding an organisation

Starting a business requires a lot of planning. There are processes from the beginning such as company formation, various registrations of the company, arranging the right bank account, filtering through the funding options and setting you your accounting system. Purple Lime, having been through the process with a lot of existing clients, has ample experience to ensure you start on the right foot.

Annual accounting

Your annual accounts are used by HMRC to work out your tax payments for the year, so it is critically important to make sure they are accurate. You work hard for your money, so you don’t want to overpay tax when you don’t need to. Making sure you have detailed records for the financial year and that you stay compliant with all the rules and regulations can be vital to paying only what you owe.

Taxation planning and compliance

Taxes come in all shapes and sizes, and planning throughout the year can ensure you pay the right amount at the right time. Our modern accountants are always up to date with the latest changes to the tax system and will help you maximise the profit your business makes.

Staff and payroll

Such a large part of a business’ overheads are the staff costs, not to mention the time this complicates process consumes. Why not leave it to experts such as Purple Lime who will ensure payroll, pensions, HMRC compliance, changes of staff and reports will be done on time with instant access for you? We will ensure that you receive the benefits you, as a business and as an individual, are entitled to.

Financial systems implementation, training, and education

Xero accounting software makes it easier to keep track of your business finances while you’re on the go, but problems can waste time and money. Choosing a Xero Gold Champion Partner means our expert accountants can assess your current system and provide training and support to make your processes smoother.

Registered office services

There are a few added benefits of having your Company Secretarial services with Purple Lime. Having the prestigious address in Corsham, Wiltshire, and access to the facilities offered by the grand setting of the Hartham Park mansion. Some of the other advantages are the removal of your personal address from public record and post handling on your behalf, saving you valuable time. Further business services available as well as a full virtual office. Your information will be safe with us.

Custom engagements for every client means you pay only for what you need.

Up to 75% off ReceiptBank through us*.

Discounted software fees with us.

*Discounts applied when signing to our specific services compared to stand-alone subscriptions.

")

To find out more about how we can help,

call us on 01249 263 333 or book a FREE consultation

Integral to your business

Seamlessly running your finance department

Many businesses are looking for more from their accountant than just dropping a box of receipts off at the end of the year. Most businesses recognise that it is better to outsource or seek the support of accountancy experts, who can help to guide and support the business from an external position, to help them make the right decisions for their business at the right time.

Accountancy services

Sometimes it’s easier to hand a task to the experts. Whether it’s looking after your bookkeeping, Xero setup or other stand-alone tasks.

Support & Xero training

You may do most of your accountancy yourself or through your in-house team, but sometimes you may need an expert opinion or Xero training for you or your staff.

Dedicated finance team

Outsource all your accounting and feel assured that the experts are looking after every aspect of your business finances.

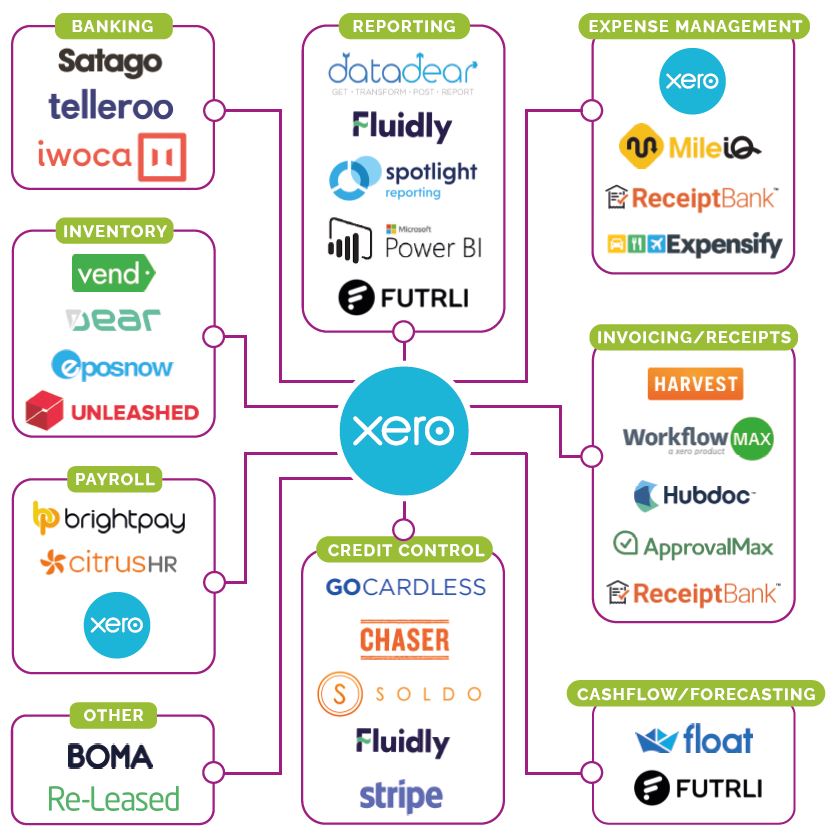

Xero ecosystem

Improving efficiency with Xero.

Xero is the UK’s leading cloud accounting software and is used by over 2 million businesses worldwide. You can have access to real-time account information from your Mac, PC, tablet or phone giving you greater control and the ability to make better decisions.

Xero connects with over 700 different time-saving apps so that you can easily sync and streamline your data. From inventory management, invoicing and time tracking, there’s everything you need to grow your business.

If you want to make the move to Xero, or need some training to use it to its full potential, speak to our specialists today.

If you have a question please call us on 01249 263 333

Some feedback from our clients

I am really happy with the service that Purple Lime are providing to Silver Bullet. Outsourcing our finance function allows our business to remain lean and focussed on delivering value to our clients whilst we scale.

Engaging with Purple Lime was an easy process and their use of cloud technology meant it wasn’t long before we saw the value of their output. This is by far the best accounting firm we have worked with, so I pass on my thanks to the team!

We had a number of accountants and advisers before meeting Purple Lime and can now say with certainty we have found the right accounting partners to help us move our business forward. Working with the Purple Lime team is great.

Our accreditations